Where Good Intentions Meet Poor Outcomes: The Urgency of Reimagining Personal Finance Education

- Jeff Hulett

- Mar 18

- 5 min read

Updated: Mar 21

In classrooms across the country today, a quiet revolution is gaining momentum. As recently highlighted in the Wall Street Journal, state legislatures are rapidly mandating financial literacy as a high school graduation requirement. This surge in legislation is born from a noble recognition: wealth inequality is reaching historic highs, and families are clamoring for their children to be better equipped for a modern economy.

However, we are approaching a dangerous intersection where well-meaning policy meets fundamentally flawed execution. Decades of data, including a landmark meta-analysis of over 200 studies, have revealed a startling truth: traditional, information-based financial education has a near-zero correlation with actual financial success later in life. These "facts-first" interventions often see their meager effects wither away within a mere 20 months.

While these new laws are well-intended, they risk making financial outcomes worse by scaling a broken model. The shift of personal finance to a core graduation requirement—on par with Math and English—is historically significant. But if we simply provide "more of the same," we are setting students up for failure. We must move past the "Information Accumulation" trap and adopt a Behavioral and Decision Model that prioritizes repeatable judgment over perishable facts.

The Trap of Information Accumulation

The core problem is that personal finance is often taught as an information accumulation problem. While core language acquisition and literacy are the vital foundations of education—the "alphabet" of learning in the lower grades—financial education must build upon that curriculum to create a framework for action.

In the legacy model, success is measured by a student’s ability to memorize definitions or calculate interest rates by hand. This "facts-first" approach assumes information is a scarce resource. But in the modern age, information is not scarce—it is a flood.

Teach Personal Finance Like We Teach Nurses

Teaching personal finance through rote memorization is like training a nurse with textbooks but no clinicals. We force students to memorize formulas their AI can recite instantly, then wonder why they 'bleed out' when facing real-world predatory loans. 'Book smarts' without simulation leads to fatal errors—in medicine and in money.

Flooding a consumer with more data without providing a framework to process it does not lead to wealth; it leads to paralysis, a reduction in confidence, and ultimately, poor choices. When we reduce personal finance to rote memorization, we ignore the reality that financial success is not about what you know, but how you decide. True financial literacy is a decision problem, yet we continue to teach it as an information problem. We must move beyond simply teaching the "language" of money and start teaching the "logic" of the decisions made with it.

"God only knows what it's doing to our children's brains."

- Sean Parker, founding president of Facebook

The 'Like' Replaced Lighting up

Rather than viewing Big Tech through a moral lens of "good" versus "bad," it is more useful to recognize it as a force stretching our evolutionary biology to its limits. The human brain was not engineered to navigate a landscape of information abundance and attention scarcity.

Big Tech influences our neurobiology by targeting reward-driven dopaminergic pathways. This mirrors the nicotine addiction strategy used by Big Tobacco in the mid-20th century. By shortening attention spans, these platforms aim to bypass “slow” thinking to induce immediate "Buy Now" actions.

Education serves as the bridge between our biological hardware and the modern digital environment. While Personal Finance education can provide a "Better Way" to counter these strategies, it must be taught with an understanding of how consumer platform systems exploit our evolutionary biology.

The Architects of a New Way: A Highly Credible Coalition

To achieve better outcomes and increased agency, we must look to a new approach: Personal Finance Reimagined (PFR). This system was built by a highly credible, experienced, and diverse group of experts who recognized that the traditional curriculum was broken.

Led by Jeff Hulett, a personal finance professor at James Madison University, a behavioral economist, and a veteran banking executive, the PFR team is a motivated coalition of:

Long-time Educators: Pedagogy experts who understand that student engagement is the first step to learning.

Behavioral Economists: Scientists who study the cognitive biases and our default decision systems—that lead people to make irrational financial choices.

Technologists: Specialists who have developed student-focused choice architecture, the technology of behavioral economics. The "Definitive Choice" app is a simulation-focused engine awarded two U.S. patents.

Consumer Protection Regulators & Bank Executives: Industry veterans who have spent decades inside the systems that govern how money moves and how consumers are protected. They know the "dirty little secrets" of the industry and are committed to helping people find a new path.

This team didn't just write a new textbook; they built a new financial education architecture.

The System as the Hero

As a teacher, receiving positive feedback is what keeps me motivated. Hearing a student like Jada L. say, “Professor Hulett is hands down one of the best professors I’ve ever had. He deeply cares about the material and delivers it excellently.” is deeply inspiring. However, the real hero of this success story is the teaching system itself. It is the system making me look good and motivating me to be good.

For too long, instructors have felt tethered to outdated curricula geared toward the world as it was. It is a frustrating experience to be required to focus on memorization and manual calculations when the world has moved on to AI and instant data. This legacy approach forces teachers to be conduits for "facts" that are often obsolete by the time a student graduates.

The PFR system changes the role of the teacher from a lecturer to an orchestrator. It aligns the classroom with the world as it is and will be. By utilizing Generative AI as a "Decision Architect’s Assistant," the system helps students curate the flood of modern data without sacrificing human agency. When a teacher uses a system that integrates behavioral science and real-world simulations, they are no longer just teaching a subject; they are practicing a practical survival guide for the 21st century. This alignment makes teachers feel more connected to the future, rather than anchored to the past.

Proven Results for a Scalable Future

This methodology isn't just theory; it has been rigorously tested in universities and high schools with transformative results. Currently, 97% of students who have gone through the PFR system say they would recommend the course to a friend. They cite "real-life application" as the reason—not because they enjoyed a math test, but because they gained a consistent, repeatable decision process.

The approach has earned the endorsement of global leaders like John List, the Kenneth C. Griffin Distinguished Service Professor in Economics at the University of Chicago. List describes the "decision process-first focus" as a "personal finance game changer," noting that a repeatable process is an essential step for making personal finance education a "scalable success."

As state laws continue to mandate financial literacy, we face a critical choice. We can continue down the path of well-intended but ineffective information dumps, or we can embrace a science-based, technology-enabled system. The path to closing the wealth gap lies in an education that turns financial confusion into confident, lifelong wealth-building. We have the proven team and the validated results. It is time to stop teaching personal finance as a history of the past and start teaching it as a decision for the future.

For more information on our Financial Education pedagogical research and results, please see:

Student Success -> Shared Success

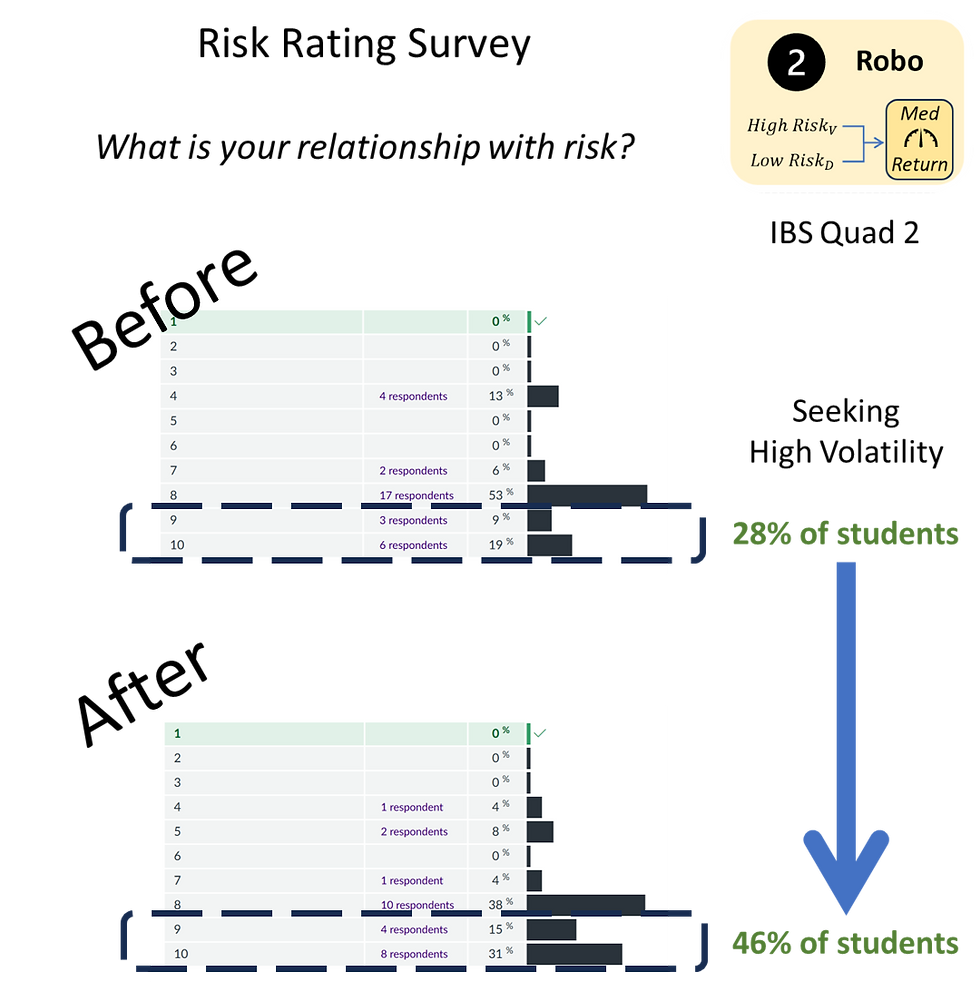

Risk Attitude Results -> Moving The Needle: The Value of Financial Education & Improving Our Relationship With Risk

PFR Pedagogy overview -> The PFR Pedagogy: How We Practice Getting Rich

College Student Investment Attitude Test Results -> Case Study: Quantifying the Impact of Process-Driven Risk Education on Investment Behavior

High School Curriculum research -> Elevating Financial Education in Virginia: A Decision-First Approach for a Data-Rich World

Great article! Thanks Prof. H for taking this on.